Buyers: Affordability just improved—lower repayments may boost your borrowing capacity.

Sellers: Expect more enquiries as confidence builds, especially in entry-level and family segments.

Investors: Cheaper credit plus steady rents mean stronger yields; timing your purchase before prices lift could pay off.

Homeowners: Refinancing could save thousands annually; talk to your bank or broker about rate options.

OCR slashed to 2.5%—biggest cut in years.

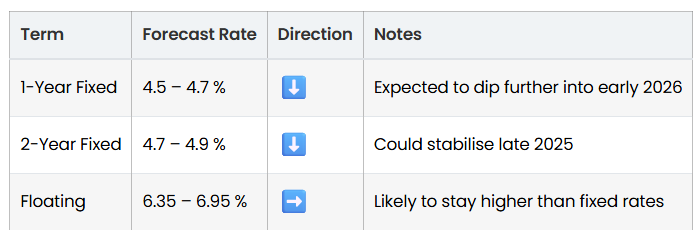

Mortgage rates dropping towards mid-4% range.

Housing demand rising as affordability improves.

Price growth forecast: 2-3% over 2025.

Best window to refinance or buy before rates stabilise again.

Economist Tony Alexander says the jumbo OCR cut is “a clear signal the Reserve Bank wants households to spend and businesses to invest again.” Kiwibank economists add that “lower rates will revive housing turnover through 2025, though the rebound will be gradual.”

The RBNZ’s rate cut is likely to mark the turning point in New Zealand’s property cycle. While the economy remains soft, cheaper finance, limited housing supply, and returning buyers set the stage for a moderate recovery through 2025-2026.